Treasury Secretary Jack Lew just upped the ante in a scary high stakes poker game with Republican congressional leaders over the debt ceiling. Lew warned in a letter early Thursday that the government could begin running out of cash without new borrowing authority as early as November 3 – two days earlier than Treasury’s earlier estimate.

Unless Congress and the Obama Administration strike a deal by early November to raise the $18 trillion debt ceiling, the Treasury will exhaust the extraordinary measures it has been using to keep the government operating and face the first default in borrowing and payment obligations in U.S. history.

Related: McConnell’s Last Stand: He Wants Medicare, Social Security Cuts to Raise Debt Limit

Aside from the embarrassment of being labeled a global deadbeat, the immediate results of this fiscal disaster will take a huge economic toll. Foreign debt holders would be paid first until the money runs out. Then, if we renege on interest payments owed to countries like Japan and China, rattled financial markets could drop like a stone.

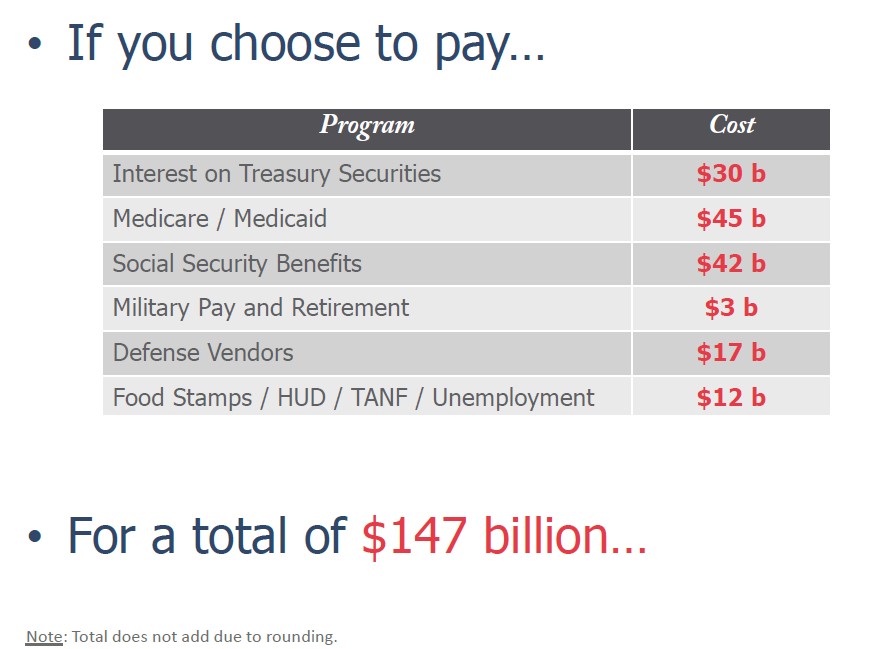

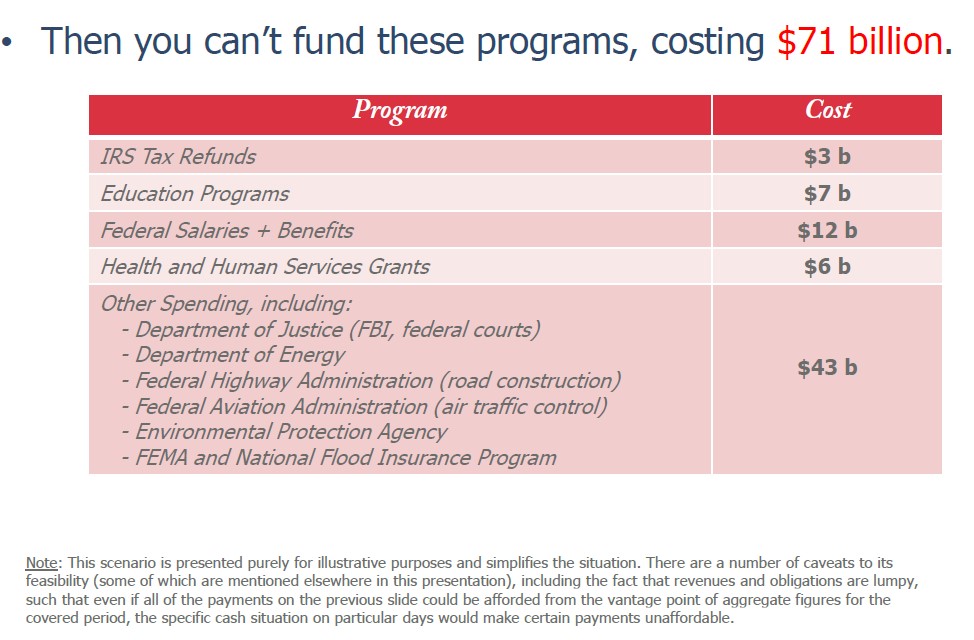

Let’s say we do everything short of putting the White House up for sale in order to pay our foreign debt holders. What about our other obligations? The Bipartisan Policy Center shows in two charts what would happen if the government prioritized spending on other obligations.

In short, the country will be unable to make many of the payments that its citizens rely on every day. As the Bipartisan Policy Center puts it, “On a day-to-day basis, handling all payments for important and popular programs (e.g., Social Security, Medicare, Medicaid, Defense, Military Active Duty Pay) will quickly become impossible.”

We’ve been down this harrowing fiscal road before, although the path seems even more treacherous this time because of all the political chaos on Capitol Hill with time running out.

Republican lawmakers and President Obama literally came within hours of a default in the summer of 2011 before reason prevailed and they cut a last minute spending deal. Standard & Poor’s was so alarmed by that mid-summer near-disaster that it issued a strong rebuke of irresponsible governance and slightly downgraded U.S. treasury notes in the aftermath of the struggle.

Related: The Debt Ceiling: What Is It And Why Should We Care?

The last time Congress hiked the debt ceiling in February 2014, only 28 House Republicans voted for it, while nearly all the Democrats had to join in to help pass the legislation, 221-201. The showdown this time could be even tighter, especially since some of those 28 Republicans are no longer in Congress.

Even if debt ceiling legislation makes it over to the Senate, Majority Leader Mitch McConnell – who long has vowed to avert a default or another government shutdown - appears to be suddenly rattled by the far right in Congress and on the presidential campaign trail who have been questioning his fealty to hard-rock conservative convictions. McConnell this week signaled a newborn insistence on linking the debt ceiling to some of the most contentious issues imaginable. According to media reports, those demands include changes to Medicare, Social Security, and Environmental Protection Agency regulations as his price for raising the nation’s debt limit.

Related: 8 Ideas for Saving Social Security Disability Insurance

There is no way, of course, that Obama and Democratic congressional leaders would agree to such changes, especially amid the highly charged presidential campaign. Even in the best of times, Congress could not pass such complex and politically fraught legislation in a matter of weeks.

Wall Street and business leaders generally try not to get too worked up about the periodic congressional battles over the debt ceiling. Despite all the heated rhetoric and maneuvering, many assume that cooler heads will prevail in the end and a deal will be ironed out. And if he has his way, Boehner will be able to point to one last debt ceiling deal as part of his legacy as he heads for the door.

But with the future leadership of the House now very much up for grabs, a sizeable block of hard right conservatives demanding major changes in the way Congress conducts its business, and a wobbly Senate Republican Majority leader who has come under relentless attack by Sen. Ted Cruz (R-TX) and Republican presidential frontrunner Donald Trump for being weak, a debt ceiling disaster may be a lot closer than many think.

“In this environment, it’s very, very difficult to get [a debt ceiling bill]. The whole weight of force is behind the people who are against the debt limit,” Francis Creighton of the Financial Services Roundtable told The Hill this week.

Related: Debt Ceiling Drama: Will You Get Your Tax Refund on Time?

With Congress in recess for a week, there is no sign of negotiations on spending and debt ceiling matters – although GOP leaders and the Democrats may well be conferring quietly by phone. Whether Boehner can orchestrate passage of a “clean” extension of the government’s borrowing authority at least through the remainder of the year or into 2016 remains to be seen, although conservatives in both chambers can do enough mischief to at least slow down the process until right up to the deadline.

While the Treasury, the Congressional Budget Office and the Bipartisan Policy Center have offered varying forecasts on when the Treasury will actually start running out of money, there is general unanimity that the crisis could erupt just about any time in the first couple of weeks of November.

“I think there’s agreement right now that – unless we get a debt ceiling before then – that the first ten days of November are going to be pretty tricky,” said Steve Bell, a former senior Senate Republican budget aide and a top official at the Bipartisan Policy Center.

Some Republicans believe that the Treasury may be overstating the true deadline for action and that they may be able to prolong the talks in order to extract concessions from the White House. But with so much uncertainty about the ebb and flow of tax revenues and other factors, lawmakers would be dancing on the edge of a cliff by dragging out negotiations. Bipartisan Policy Center analysts currently are pegging the likely “drop dead” deadline for action as November 10 to 19.