The baby boom generation has broken the mold at every stage of life, and it looks like old age won't be any different.

Boomers aren't heading quietly into retirement. They're launching businesses, embracing digital technology and living abroad in greater numbers than ever before. But in other ways they are struggling more than the previous generation.

Here is a look at trends shaping the next wave of retirement.

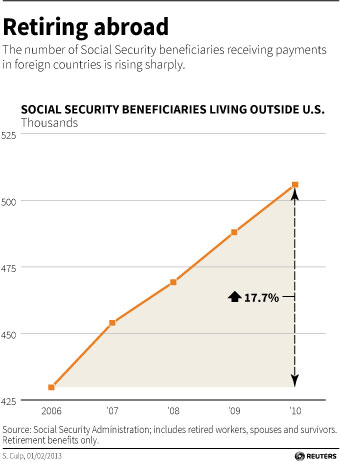

THEY ARE LEAVING THE U.S.

More older Americans are packing it in for foreign countries, where they can save on living costs and enjoy warmer climates.

The number of retired workers, spouses and survivors getting Social Security benefits in a foreign land is rising almost twice as fast as the number of Social Security beneficiaries generally, according to Social Security Administration data.

RELATED: Boomers Redo Their Homes for a Groovy Ripe Old Age

And 21 percent of baby boomers say they are "interested or very interested" in retiring abroad, according to a survey by the Center for Medical Tourism Research at the University of the Incarnate Word in San Antonio, Texas.

"If that were extended across all boomers, you'd have about 3 million people retiring abroad in the next couple decades," says David Vequist, the center's director.

THEY ARE STARTING COMPANIES

Almost a quarter - 21 percent - of new U.S. businesses started in 2011 were launched by entrepreneurs age 55 to 64, according to the Kauffman Foundation, up from 14 percent in 2007. Entrepreneurs age 45 to 54 accounted for an additional 28 percent of the 2011 startups. Taken together, that's 49 percent of all startup activity - far larger than the 20- to 34-year-old bracket, which accounted for 29 percent of new ventures.

In part, the surge can be attributed to the 2008 recession, which sent older workers into consulting gigs. However, there are a surprising number of complex, sophisticated and large businesses being created as well, according to Dane Stangler, director of research and policy at the Kauffman Foundation. He also thinks many of these older business owners are "serial entrepreneurs."

"We're seeing a lot of entrepreneurs in fields like technology and engineering who are launching substantial businesses," he said. "They started companies in their thirties or forties, and now they're doing it again."

THEY ARE TECH SAVVY

Young people might be leading the digital revolution, but boomers - the generation born 1946 to 1964 - aren't far behind.

"Baby boomers got quite comfortable with the Internet and other digital technologies in the workplace," says Lee Rainie, director of the Pew Internet Project. "They won't give that up as they age."

For example, 23 percent of older boomers and 27 percent of their younger siblings use tablet devices, compared with 30 percent of Gen Xers (born 1965 to the early 1980s), according to the Pew Internet Project. The gaps also are small when it comes to smartphones and social networking services.

"They're not going to be downloading every new app that catches the crowd," he says. "They're very utilitarian - show me how it will work for me, how it will improve my life." Expect retiring boomers to publish creative works online, connect with friends and children via social media and continue to job-hunt on sites such as LinkedIn.

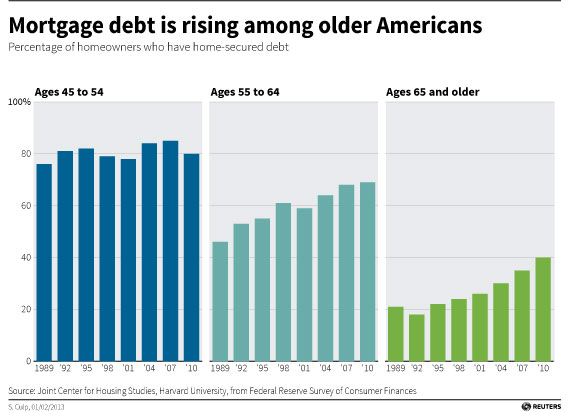

THEY ARE BORROWING MORE

Older Americans are taking more debt into retirement than previous generations. Mortgage debt is the biggest factor: Forty percent of homeowners over age 65 had mortgage debt in 2010, compared with just 18 percent as recently as 1992, reports the Joint Center for Housing Studies at Harvard University (JCHS).

The culprit: the refinancing boom before the housing crash. In the years leading up to 2008, homeowners took advantage of low rates and deductibility of interest to refinance, says Lori Trawinski, senior strategic policy adviser at the AARP Public Policy Institute.

"(They) took out equity for things like education or a new car," says Trawinski. Boomers on the cusp of retirement are still refinancing, sometimes at the behest of their financial advisers, because of the appeal of today's near-record-low interest rates.

Higher debt levels will have a variety of effects. Some retirees will be stuck in homes with underwater mortgages or monthly mortgage payments that sap their spending power; others will use low-interest mortgage debt to keep more cash on hand or to keep other money invested longer.

THEY ARE OUTLIVING THEIR EXPECTATIONS

Life expectancy for men has jumped an average of almost two years in each of the last five decades, to 75.7 years in 2010, according to the Society of Actuaries. For women, life expectancy has risen by 1.5 years, on average, to 80.8 years.

Yet more than half of older Americans haven't gotten the memo. A Society of Actuaries survey of 1,600 adults age 45 to 80 found 40 percent underestimated their likely average longevity by five years or more; 20 percent were too pessimistic by two to four years.

"That means there's a 50 percent chance you'll live longer," says Cindy Levering, an actuary and co-author of the report. "If you make it to 90 and only planned and saved enough for 85, you may not have enough to live on."

The odds that will happen are pretty good. For a couple with above-average health, there's a 60 percent chance one of them will live to age 90, the Social Security Administration has reported.

THEY ARE PROVIDING FINANCIAL SUPPORT

Some 58 percent of boomers are providing financial assistance to aging parents, such as helping them purchase groceries or pay medical and utility bills, according to an Ameriprise Financial survey of just over 1,000 Americans conducted in late 2011.

When it comes to their kids, boomers are even more ready to help out.