On the surface, you’d suppose that there would be a big difference between Apple’s first bond issue in 17 years and the debt that the Treasury sells on a regular basis – carefully marked down on the calendars of traders and investors – to finance the government’s spending programs. After all, one is a profitable business that is still growing, even if at a slower pace than it has in the last decade or so, while the other is a bureaucracy that, far from making a profit, generates budget deficits year after year after year.

And yet... the debt that Apple is selling yields so little – at 20 to 100 basis points above the ultra-low yields on government bonds – that it begs comparison with Treasury debt. Investors flocked to buy the Apple debt issue: it offers a not-too dissimilar range of options and characteristics. In the eyes of some investors, it may even be playing the role of a ‘safe haven’ bond investment.

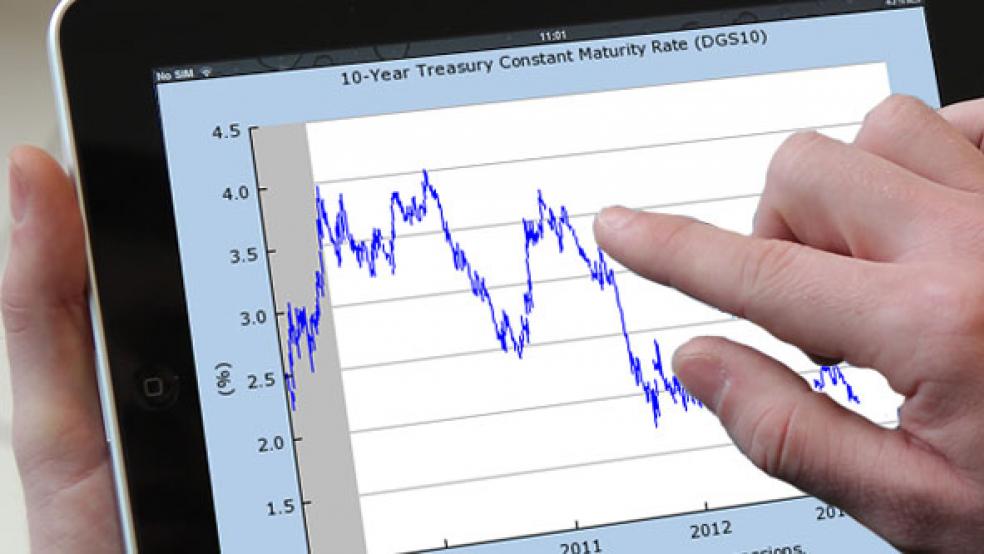

Among its six-part, $17 billion offering, Apple reportedly sold $5.5 billion in 10-year debt at an annual yield of 2.415 percent. Compare that to 10-year Treasuries, which now yield just over 1.6 percent. (It should be noted that Microsoft issued $1.95 billion in debt last week at slightly lower rates.)

So, given that you have the option of owning what likely will be the ultra-liquid bonds just issued by Apple (in what is the largest non-financial corporate debt sale on record) or the slightly more liquid but slightly lower-yielding Treasury bonds, which should you pick?

Let’s take a brief look through some of the fundamental considerations.

Credit Rating: Standard & Poor’s doesn’t see much difference between the U.S. Treasury and Apple when it comes to credit quality: both fall shy of AAA status, winning AA+ ratings, the second best that the agency doles out. Worth noting, however, is that Apple’s rating has improved from junk bond status in the late 1990s to this stellar rating today, while the U.S. government famously lost its coveted AAA rating in the summer of 2011. My view? The Treasury wins here, but only because it can levy taxes to meet its obligations, while Apple can’t force people to buy its iPhones.

Business Risk: What business risk can the U.S. government have, you ask? Well, plenty – just look at the “sequester” and the ongoing battle over fiscal priorities in Washington. That’s business risk, in a nutshell, even if it isn’t as straightforward as the kind on display at Apple, which has been grappling with the fickle nature of consumers’ affection and shoppers’ quest for the next great innovation that can rank alongside the iPhone and the iPad. My view? Apple has the edge: Folks have been trying to get elected officials to behave rationally for generations, largely in vain.

RELATED: The Biggest Threat to Apple: Samsung or Google?

Governance: Much the same as above. When President Obama is asked by a reporter whether he has the “juice” to see through his political agenda in Congress, you know there’s a problem. And let’s face it, Apple CEO Tim Cook doesn’t have the same charisma or tech-world gravitas as Steve Jobs possessed. In both cases, there’s a hefty chance that their critics could be wrong, of course. My view? The corporate governance structure is set up to appeal, explicitly, to potential investors and to address the concerns they may have, while the government’s responsibilities are more varied and thus harder to manage. This gives Apple the win in this category.

The Financial Picture: This is a far more straightforward category. Apple is sitting atop a cash mountain amounting to some $145 billion, although most of this is held offshore and can’t be repatriated to the U.S. without incurring a large tax hit. Technically, the only reason that Apple is issuing the bonds is that it doesn’t want to take that hit: It could readily finance everything it wants to do from its own coffers, if it chose. Discussing its AA+ rating on Apple, S&P commented that this reflected its belief that “Apple will maintain very modest leverage, significant net cash balances and a commitment to a minimal financial risk profile.” Compare that list of characteristics to what might be said of the U.S. Treasury, which has to keep rolling out the bonds in order to keep the Social Security checks rolling off the presses. My view? Apple, by many, many lengths.

This doesn’t mean that there is no place for Treasury securities in your portfolio. The U.S. government, for all its flaws, is a strong bet to still be around in 30 years. Apple, which just turned 40 last month, is likely to be a far different company three decades from now, assuming it’s still around. Getting about one percentage point over Treasuries for that kind of long-term bet makes the risk/return picture on these bonds look questionable.

Of course, the ideal security to own right now would be some kind of convertible bond. Unless you are convinced that Apple has lost its mojo (in which case, why would you even be considering investing in its bond issue?) such a security would have offered investors the perfect win-win: current income and a call option on the upside potential in the stock price. That would have appealed to investors too wary of the slackening growth rate to dive back into the stock with the same amount of gusto they displayed for the bond issue. No luck for investors this time around, alas.