The Dow Jones Industrial Average has fallen below the 17,000 level again while the Russell 2000 looks set to confirm a scary looking five-month downtrend pattern. The bulls have stepped in again. If they hadn’t, or if their push upward fails, we could be looking at a revisit of the late September lows.

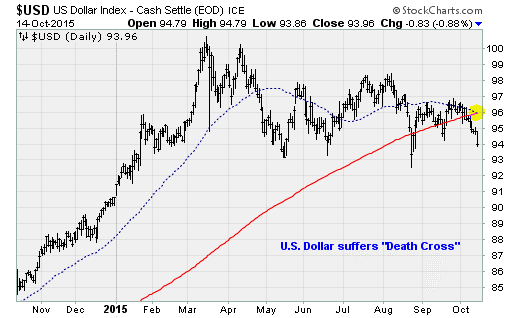

The renewed buying appears to be happening thanks to this: An accumulation of bad news has pushed the U.S. dollar onto the precipice of a "death cross" — or a move of its 50-day moving average below its 200-day moving average — for the first time since 2013.

Related: Why We Might Be Headed for a Recession in 2016

I know that all sounds terrible. But it's actually great and has helped Asian markets surge on Thursday morning while juicing U.S. equity futures. Here's why. The accumulation of bad news, according to Federal Reserve mouthpiece Jon Hilsenrath at The Wall Street Journal, has lessened the odds of a rate hike this year. In fact, futures market odds now put the chance of a March 2016 rate liftoff at about 50-50.

As a result, a chain reaction has been set off, bouncing from currencies to commodities to stocks, that looks set to undo some of the negative dynamics that have been in play since stocks stalled as crude oil cratered in the summer of 2014.

In order for this to happen, the fundamentals needed to worsen. Which they have.

Stocks dropped on Wednesday in response to weaker-than-expected guidance from Wal-Mart (WMT) and a disappointing retail sales report that called into question the health of the consumer and cast further doubt on the health of corporate earnings as the Q3 reporting season rolls on.

Wal-Mart stock fell 10 percent to close at $60.03, on Thursday it dropped below the $60-a-share threshold last crossed in 2012. Management said fiscal 2016 sales would flatline, with fiscal 2017 earnings per share declining between 6 percent and 12 percent despite the approval of a $20 billion share-repurchasing program worth 10 percent of its market capitalization. The problem is rising wages: 75 percent of the earnings reduction is due to wage increases.

On the economic front, it was all about evidence of slowing demand. Headline monthly producer price inflation sank into negative territory in September for the first time since April; the year-over-year rate posted its eighth consecutive month in negative territory. The headline number was dragged down by a 5.9 percent drop in energy prices and a 0.8 percent drop in food prices.

Also, the September retail sales report was weaker than expected, with total sales less autos down 0.3 percent month-over-month.

All of this comes in the wake of that underwhelming September jobs report in which non-farm payrolls expanded by just 142,000 — below Wall Street's lowest analyst estimate.

Related: Not So Fast, Janet — Why the September Jobs Report Really Matters

While the logic seems backward, the bad news is good news for stocks — especially for beaten down areas of the market sensitive to the dollar's rise and the drop in commodities, such as energy, industrials and materials. The inflation trade is back on.

Indeed, these are the areas that led the overall market out of the late September low, leaving recent leaders such as big-tech and biotech in the dust — so much so that Goldman Sachs noted the momentum reversal was a historic neck-snapper: According to their calculations, such a rapid change in the market's vanguard has occurred less than 1 percent of the time since 1980.

No surprise then that investors are piling back into precious metals as everyone realizes the Fed isn't likely to move on policy tightening until higher inflation is staring us in the face.

WTI Crude Oil Spot Price data by YCharts

Because of the math behind inflation measures, which have been weighed down by the drop in crude oil prices, things could quickly turn around should crude climb back toward the $60-a-barrel level by the beginning of December.

The year-over-year consumer price inflation growth rate would snap back, fueling concerns the Fed was duped by the data and has fallen behind the curve. Gold and silver, which have been out of favor since 2012, would become the latest objects of speculative desire should the Fed really wait until the middle of 2016 before raising rates. The groundwork is being laid.

Related: A Cautious Fed Sets Stage for Epic 'Santa Claus' Rally

On Wednesday, the Gold Trust SPDR (GLD) surged 1.7 percent to move above its 200-day moving average for the first time since May — a level it hasn't been able to stay above, in a sustained way, since January. It also boosted the Market Vector Gold Miners ETF (GDX), which tracks a basket of gold mining stocks including Goldcorp (GG) and Newmont Mining (NEM), by 6.5 percent. I expect these runs to continue.

This should also translate into support for the stock market as the Russell 2000 reaches a critical "do-or-die" point: Either it blasts up and over its September resistance or succumbs to the downtrend pattern in place since June with a retest of last month's lows.

My guess: Dovish commentary from the Federal Reserve and other global central banks ignites a multi-month rally led by recent laggards in areas like industrials, energy, materials and precious metals.