On the surface, the threat of high inflation is probably the last thing worrying average Americans. Instead, you're probably worried about the bloodlust of Islamic State terrorists. Or maybe Russian nuclear submarine patrols off our shores. Tepid wage growth. Ho-hum home price gains. The horror, depending on your political bent, of either Donald Trump or Hillary Clinton in the Oval Office.

Inflation just isn't a clear and present threat: Producer price inflation has been cratering, dropping at a 1.6 percent annual rate in October on a persistent drop in food prices. On Monday, wholesale gasoline futures tested down to $1.20 a gallon — a level not seen since early 2009. Copper and crude oil are similarly weak. Other measures, from China factory gate prices to U.S import prices, all tell the same story.

Related: Paris Attacks Add a New Reason to Fear a Market Meltdown

But a closer look at the economic data reveals something is stirring on the price front that will soon attract growing attention. In fact, with the core Consumer Price Index growing at a 1.9 percent annual rate, as the Bureau of Labor Statistics reported Tuesday, inflation is already within a hair of the Federal Reserve's 2.0 percent target.

Investors in the bond market are starting to bet with real money that inflation should stabilize and move higher despite the recent bout of commodity price weakness. According to the team at Capital Economics, the 5-year/5-year forward inflation swap rate has increased around 15 basis point to 2.2 percent since the beginning of October, despite a nearly 10 percent drop in the price of crude oil.

In their mind, this reflects an expectation that the drop in energy prices "has less to do with U.S. economic growth prospects and more to do with the greater supply of oil." Price expectations have proved similarly durable in the Eurozone as well.

Federal Reserve Vice Chairman Stanley Fischer noted in comments last week that he expected downward inflation pressure caused by the slide in energy prices to fade in the months to come as year-over-year comparisons for crude oil become easier.

Related: Can Consumers Keep the U.S. Economy Going?

Capital Economics analysts also dismiss the scary October decline in producer price inflation as driven by one-off factors, and they note the persistence of services inflation (vs. price deflation in goods) as well as evidence of coming health care and housing price inflation.

On the housing front, the decline in rental vacancies over the past year suggests that rent inflation (running at a 3.7 percent annual rate) should accelerate in 2016. On the health care front, Capital Economics project the PCE medical inflation rate to increase from a 0.6 percent annual rate in September to a 1.5 percent rate in 2016. Prices of medical care services jumped by a remarkable 2 percent in October, according to Tuesday’s BLS data.

Because of a projected inflation rebound, Capital Economics believes that the Fed will push its policy interest rate from near 0 percent now toward 2.0 percent over the next year. That estimate is far ahead of where the futures market is, with market-based estimates not predicting rates that high until the end of 2018.

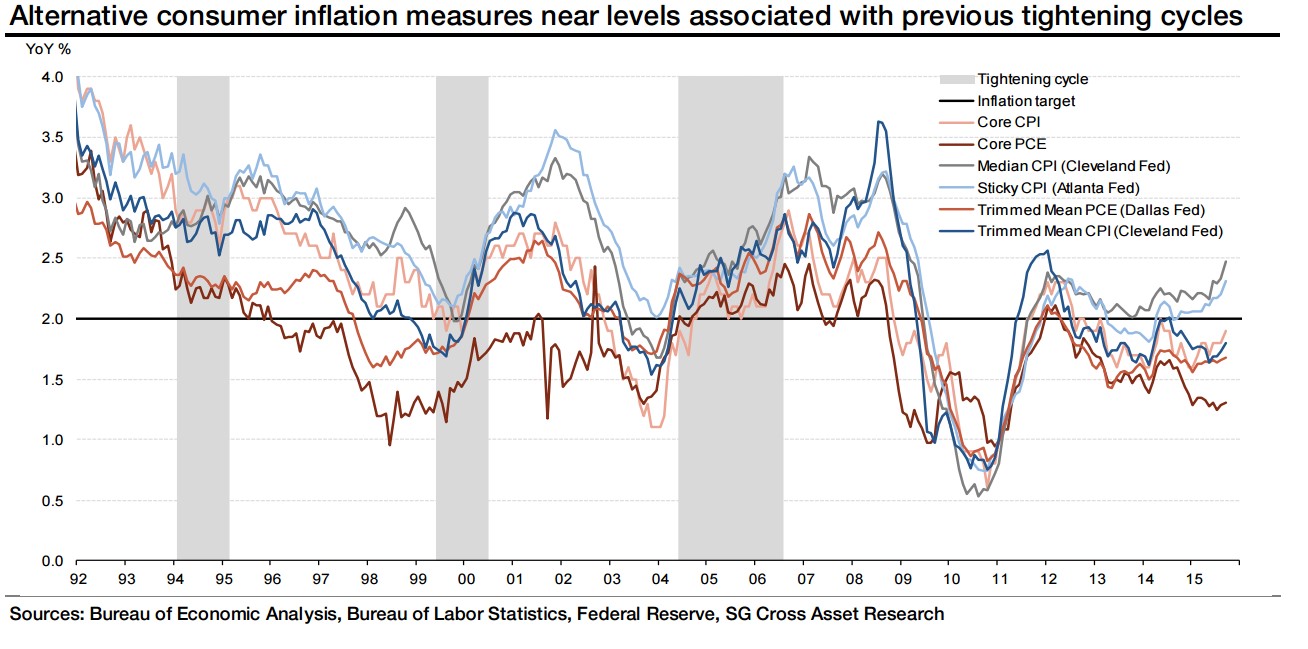

Yet Capital Economics’ analysts aren't alone in their hawkish outlook. Brian Jones at Societe Generale recently told clients that the Fed's inflation goal "is closer than you think," highlighting the turnaround in alternative measures of price inflation, as shown in the chart above, to levels that have in the past been associated with rate-tightening campaigns.

Related: Why the Fed Must Banish the 1970’s Inflation Devil Before Raising Rates

Michael Hanson at Bank of America Merrill Lynch recently declared that global policymakers are winning the "war against deflation," because of base effects, or the way low inflation last year means that even fairly small price increases this year will push the headline inflation rate higher.

And finally, Goldman Sachs is predicting the Federal Funds policy rate will hit 2.4 percent by the end of 2017 as the U.S. economy is expected to continue to grow faster than its 1.75 percent "potential" growth rate, resulting in increased pressure on wages and core inflation (especially services).

Yet despite a recent firming of bond-market inflation expectations, Wall Street just isn't prepared: By Goldman's estimation, current pricing in the inflation options market suggests risks are skewed to the downside, with a 35 percent probability that overall inflation averages less than 1.0 percent over the next five years.

This pessimism could create profit opportunities for investors in beaten down, inflation-sensitive areas of the market such as gold and silver and precious metals stocks.

Jason Geopfert at SentimenTrader has recently noted the extreme selling pressure hitting gold and silver over the past few weeks. Silver futures, for instance, declined for 13 consecutive sessions through Monday — something that hasn't been seen in 50 years of market history. In order for the Fed to declare victory, prices need to rise. And once that happens, gold and silver will shine again.