Many experts agree that natural demographic changes and lifetime income cycles distort common income inequality measurements in the United States. In short, there are a lot more middle-aged and old people now than there used to be (109 million), and older people by in large have more money than their younger counterparts, (66 million) because they have been earning money longer. And therein lies the main reason why income inequality appears to be exploding. Old people are certainly to blame, while they are paradoxically not at fault.

Economists Ingvild Almas and Magne Mogstad have established a method to adjust mainstream income inequality measurements for age differences and associated variables like education. They found that after these adjustments are made, the Gini-coefficient—a measure which underlies most contemporary academic work on income inequality—is grossly exaggerated. Their rigorous analysis is luckily quite intuitive. A 70-year-old man who has been saving most of his life, owns a home, receives Social Security payments upon retirement, and has benefited from a long-term build-up of career skills and connections leading up to retirement is going to have far more money than a 30-year-old man.

And, rest assured, there are many more old people than there used to be, meaning that their accumulated incomes skew income inequality measurements drastically. The median age in the United States rose 28 percent from 1940 to 2010 because there was a huge uptick in births in the 1950’s, and the birth rate as well as the death rate have fallen dramatically. There are more of them, and they are living longer.

Related: Income Inequality Eases, but the Middle Class Isn’t Feeling It

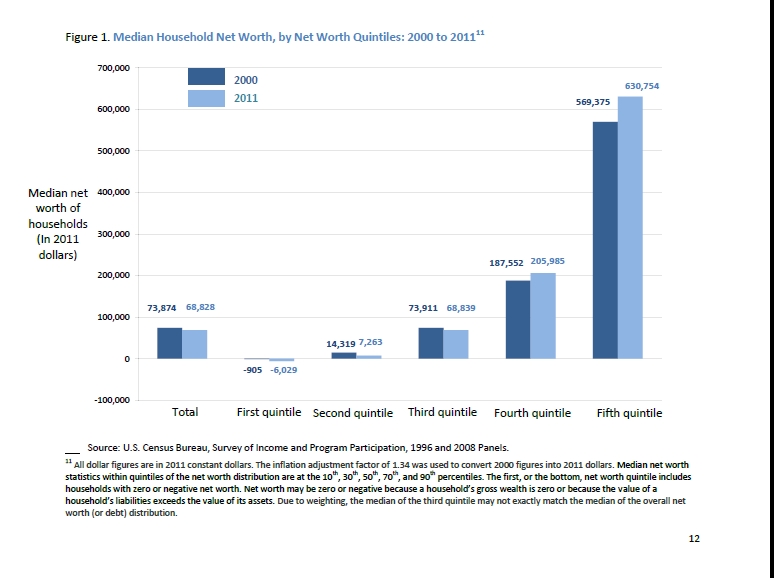

With few exceptions, U.S. Census data from 2000 to 2011 show a clear relationship between age and the median net-worth of people in every quintile, meaning that regardless of socio-economic status older folks are able to accumulate more assets over time in addition to receiving transfer payments through Social Security.

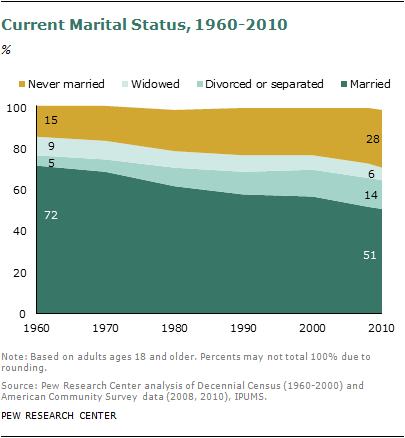

Data from the Centers for Disease Control and Pew Research Center also suggest millennials are waiting longer to marry, which in-part accounts for their lower incomes. This trend has multiple, complex causes and affects income inequality measurements in a variety of ways. Most importantly, there has been significant growth in single motherhood accompanying lower marriage rates, which has set up many young women and their children for dimmed economic opportunity and lower incomes.

Many young people are also choosing to take on debt to invest in a car, a home, and a college degree. In theory, these investments pay off in the long-term as the young become the old and advance in their careers having obtained an education and a stable living situation. This is why, for example, young people have less retirement savings than old folks. It is also why older people have far higher homeownership rates.

Related: The Middle Class Is Doing Just Fine and Still Driving the U.S. Economy

Dartmouth Economics professor Annamaria Lusardi and her colleagues have found that generational habits such as thriftiness do not matter that much in relation to productivity gains that are accrued overtime. As a whole, older people have more maturity and work experience and thus are more highly coveted by businesses which naturally offer them higher wages than their younger coworkers. One could perhaps argue that today’s grandpas spend their money more wisely than their sons and daughters, but this judgment is normative and inconsequential.

Similarly, many academics now recognize it is problematic to categorize young families as impoverished in the same way one categorizes households headed by old or middle-aged individuals as impoverished. This is because poverty in the U.S. is often only temporary. For example, according to the U.S. Census Bureau, “While 29 percent of the nation's population was in poverty for at least two months between the start of 2004 and the end of 2006, only 3 percent were poor during the entire period.” It is not hard after all for a young adult to fall into poverty or choose to live with their parents during a short period of unemployment or brief tango with an illness.

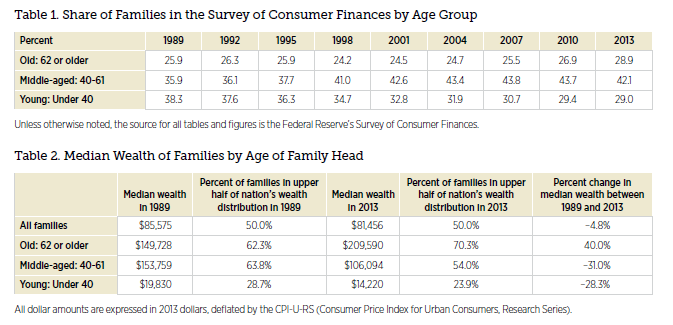

Economists at the St. Louis Federal Reserve Bank also found -- using the Federal Reserve’s Survey of Consumer Finances – that from 1989 to 2013 the median wealth of families rose 40 percent for people over the age of 62 and decreased roughly 30 percent for people under the age of 62. This indicates our economy is naturally structured to reward workers for increased experience as they age because, in the aggregate, they are considered more productive employees.

Moreover, the Federal Reserve’s low-interest rate policy, which was only recently modified, has propped up stock market growth, primarily benefiting wealthy and older households. The United States has been experiencing the third longest bull market stock surge in history, which feeds concerns that America’s wealthiest benefit the most from these massive gains while middle-class incomes stagnate.

America’s middle-class began pulling out of the stock market in 2007, which has left an even larger portion of these investments gains to high-income individuals. Stock is also disproportionately owned by older Americans, reflecting the well-established trend that people approaching retirement age have accumulated a higher net-wealth in assets like stock.

Related: Clinton Seeks Surcharge Tax on Wealthiest Tier of Americans

Government spending and debt also contribute to income inequality. After all, the Federal Reserve is pursuing low-interest rate policies because government spending, which is set to grow over the next decade, will put upward pressure on interest rates. Over the next decade, the nonpartisan Congressional Budget Office indicates that the interest rates on domestically owned debt will nearly triple, meaning the benefits older households accrue from Washington’s spending will add to income inequality.

Social Security benefits, specifically those offered to retirees, are also fueling the perceived income inequality gap between Americans with the lowest-earnings and Americans with the highest-earnings. This is because life expectancies have notable disparities based on one’s socio-economic background.

A 2015 report by the National Academies of Science, Engineering and Medicine concludes that across genders “life expectancy gains have been larger for higher earners than lower earners,” and that this reality means that people in the highest income quintiles are able to collect more social security because they are living longer than their less well-off counterparts. The report found that means-testing Social Security by lowering the “initial benefits for the top 50 percent of earners” eligible for retirement benefits would substantially decrease this income distribution gap.

As the baby-boomer generation becomes eligible for retirement benefits and reaps the rewards of their accumulated savings, income inequality will appear worse over time. While obviously not all senior citizens are well off, it is clear that demographics coupled with an awkwardly structured Social Security system are primarily to blame for the nation’s perceived income disparity.

This article was originally published in Economics-21, a website of the Manhattan Institute.