| | | Amid Protests and Pandemic, Congress Faces a $1 Trillion Fiscal Cliff

|

|

| The nation is being rocked by protests, grappling with endemic racial injustice and still struggling to cope with the ongoing coronavirus pandemic and its fallout. As disturbingly turbulent as the situation is, The Washington Post’s Jeff Stein and Erica Werner warn that the toxic stew of troubles now boiling over in city after city could be further catalyzed by a looming “fiscal cliff” that threatens to abruptly withdraw $1 trillion in emergency economic support provided by Congress to millions of Americans — or by the political battles surrounding the costly choices lawmakers face.

At the very least, the protests — and the political clashes they have sparked between the White House and Congress — could make it harder to avoid the fiscal cliff and address the difficult decisions it will force:

“Policymakers must decide in the coming weeks whether to extend emergency unemployment benefits for more than 25 million Americans. They face growing calls to provide billions of dollars in assistance for states and cities, even as President Trump increasingly feuds with governors and mayors. If lawmakers do not act, about $1 trillion in emergency federal aid used to stabilize the economy will disappear in the next quarter.”

Stein and Werner report that the federal government has pumped about $1.2 trillion into the economy since April, but that could fall to about $200 billion over the third quarter of the year, according to Michael Feroli, chief U.S. economist at JP Morgan. “The expiring aid risks creating a ‘fiscal cliff’ that, if not addressed by lawmakers, could arrest or reverse a rebound, economists say. White House officials and several Republicans have resisted pressure to approve more spending, but they are at odds over how to proceed, and the path forward is unclear,” Stein and Werner write.

Calls for more congressional action: “The violence, the anxiety that is taking place — we are naive if we think that it’s separable from the economic calamity we are in,” Darrick Hamilton, an economist and the executive director of the Kirwan Institute for the Study of Race and Ethnicity at Ohio State University, tells the Post. “Congress needs to do something to mitigate this pain — and at the very least not make it worse.”

Business groups also say Congress must act. “It’s important that Congress acted to support families and businesses as the economy came to a halt,” Neil Bradley, executive vice president of the U.S. Chamber of Commerce, says. “They can’t now leave it where they found it. They had to do step 1, that was critically important. They now need to do step 2 because that’s equally as important ... they can’t leave it where the bottom is, that’s not acceptable to anyone.”

Read the full story at The Washington Post.

|

|

| | A Third of Unemployment Benefits Haven’t Been Paid Out: Report

|

|

| The U.S. Treasury paid out $146 billion in jobless benefits in the three months ending in May as tens of millions of Americans lost their jobs due to the coronavirus pandemic. Although the number is massive — larger than all of the unemployment benefits provided during the depths of the Great Recession in 2009 — it’s smaller than it should have been, according to a new analysis by Bloomberg News.

Crunching the numbers on weekly unemployment filings and average claim size, Bloomberg found that total jobless benefits should have come to roughly $214 billion during that time.

“The estimated gap of some $67 billion shows how emergency efforts to boost payments, and deliver them via creaking state-level systems, are lagging the needs of a jobs crisis that’s seen more than 40 million people file for unemployment as the economy shut down,” Bloomberg’s Shawn Donnan and Catarina Saraiva wrote Tuesday.

A tough calculation: Although it’s hard to put a precise number on the shortfall — the Labor Department pushed back against the method used by Bloomberg to develop its estimate — there is general agreement that there are many people who still haven’t received the unemployment assistance they are entitled to. “There’s a lot more money that should have gone out that has not gone out,” said Jay Shambaugh, an economist at the Brookings Institution who has been studying the issue.

Bloomberg says its analysis likely provides a conservative estimate of the shortfall. Some states are still working through backlogs of unemployment claims — Texas alone is waiting to verify nearly 650,000 cases — and more than 7 million people are still owed retroactive benefits under the Pandemic Unemployment Assistance program for independent contractors.

Why it matters: In addition to the unnecessary suffering the delays are causing, the shortfall is reducing the positive economic effect that unemployment benefits are intended to provide. “On paper the U.S. strategy is very generous,” Ernie Tedeschi, a former U.S. Treasury economist now at Evercore ISI, told Bloomberg. “But that generosity on paper is meaningless if it doesn’t translate into actual money in people’s pockets when they need it.”

Diane Swonk, chief economist at the accounting firm Grant Thornton, said she is worried that lawmakers are experiencing “fiscal fatigue” as the crisis wears on, risking a falloff in aid that could prolong the recession. “We’re really talking about an economy that is going to be operating at a fraction of its capacity for a long period of time,” she told Bloomberg.

|

|

| | Private Equity Firms Getting More Than $1 Billion in Coronavirus Relief Funds

|

|

| Medical-service businesses owned by deep-pocketed private equity firms including KKR, Apollo and Cerberus have received more than $1.5 billion in no-interest loans from federal programs designed to help cash-strapped health-care companies, according to an analysis by Bloomberg News.

Although major private equity investors have been shut out of many coronavirus relief programs, they have found what Bloomberg calls a “back door” at the Health and Human Services Department, which has approved at least $1.5 billion worth of loans, based on a review of more than 40,000 loans made public by HHS.

Critics worry that the private equity firms will use the no-interest loans to buy up more health-care companies and load them up with debt, in accordance with their typical business model.

The money comes from two programs administered by the Centers for Medicare and Medicaid Services that received additional funding through the CARES Act to help companies in the health-care sector survive the pandemic, but “went instead to hospitals, clinics and treatment centers controlled by the richest investment firms as they seek to take advantage of an economic downturn caused by the pandemic to buy ailing businesses,” Bloomberg said.

CMS Administrator Seema Verma said her agency doesn’t ask loan applicants about their ownership structure. “We don’t look into ownership, what we look into is are they Medicare-enrolled providers,” Verma told Bloomberg.

No-interest loans aren’t the only way private equity is benefiting from coronavirus relief efforts, Bloomberg said. HHS has also provided hundreds of millions of dollars in automatic grants to health-care companies that have cared for Medicare patients over the last two years, including some owned by private equity, and the money never has to be paid back.

|

|

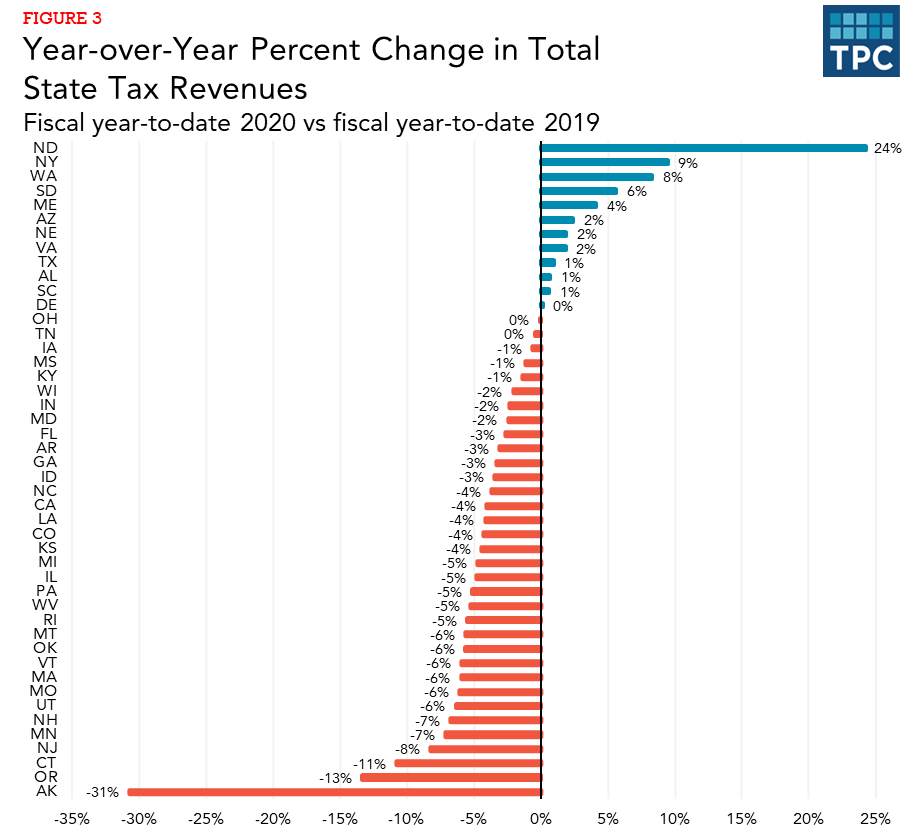

| | Chart of the Day: The Dire State of State Tax Revenues

|

|

| Lucy Dadayan of the Urban-Brookings Tax Policy Center breaks down the good, the bad and the ugly of the fiscal crisis facing states as the coronavirus pandemic crushes revenues and raises costs.

“Prior to the onset of the COVID-19 pandemic, most states were generating solid revenue growth. And many built up robust rainy day funds. But the pandemic has largely wiped out earlier revenue gains and most states now anticipate substantial revenue shortfalls for the current fiscal year and for fiscal year 2021,” she writes.

The good: Preliminary April tax revenue data show a steep drop in estimated and final annual tax payments as the tax-filing deadline got pushed back from April 15 to July 15. But taxes withheld from paychecks grew in 17 states compared to April 2019. “Tax withholding is usually a better indicator of the current strength of the economy and of the path for personal income tax revenue because it comes largely from current wages,” Dadayen explains. On the other hand, 16 states reported declines of less than 10%, while five states posted double-digits drops, so the bright spots are limited.

The bad: “Declines in sales tax revenues have been fast, steep, and widespread across the states,” Dadayen writes. How steep? April sales tax revenues fell by 16% across 42 states for which the Tax Policy Center has complete data. Twenty-three states reported double-digit declines, while just five states reported year-over-year growth. And since the April data mostly reflect March sales, the May numbers are likely to be even worse.

The ugly: For the fiscal year so far, total state tax revenue has fallen sharply — and next year is expected to be worse. “With two months remaining in the fiscal year for 46 states, total state tax revenues are now down about $57 billion, compared to last year,” Dadayen writes.

After the sharp pandemic-related plunge in April, tax revenues have fallen in 34 states compared to 2019 and risen in 12. (New York, the state hit hardest by the virus, is surprisingly among those dozen, but Dadayen says that’s only because its fiscal year 2020 ended in March, so April’s devastation isn’t reflected in the data. The state reported that net taxes and fees collected in April, the first month of its new fiscal year, fell by 69% compared with April 2019.)

|

|

| | | | | | | | - How to Make this Moment the Turning Point for Real Change – Barack Obama, Medium

- Just Stop the Superspreading – Dillon C. Adam and Benjamin J. Cowling, New York Times

- Hope Is Not a Plan, but Without a Plan, There's Little Hope – Steve Benen, MSNBC

- Trump Takes Us to the Brink – Paul Krugman, New York Times

- A New Economic Austerity Could Be ‘as Life-Threatening as the Virus Itself,’ Says Head of the National Domestic Workers Alliance – KK Ottesen, Washington Post

- The Suicide of the Cities – Kyle Smith, National Review

- An Urban Exodus Could Move the Suburbs to the Left, Not the Right – Jim Geraghty, National Review

- Dear Senate: Just Forgive the Paycheck Protection Program Loans Already – Gene Marks, The Hill

- Primary Care Doctors Could Be COVID-19's Next Victims – Drs. Tom Frieden and Dan Schwarz, The Hill

- Don’t Bar Ex-Offenders From Coronavirus Aid Funds – Cyrus R. Vance Jr., New York Times

- The FDA Should Not Rush a Covid-19 Vaccine – Steven Joffe and Holly Fernandez Lynch, Washington Post

- Conquering Coronavirus and Future Epidemics – Paul R. Michel, Morning Consult

- Understanding the Maze of Recent Child and Work Incentive Proposals – Elaine Maag and Nikhita Airi, Tax Policy Center

- The CARES Act Charitable Deduction for Non-Itemizers Was a Lost Opportunity to Help Beneficiaries of Non-Profits – Gene Steuerle, The Government We Deserve

-

Nonprofits Need Relief to Help the Economic Recovery, Too – Fred Dixon and Brad Dean, The Hill

|

|

|

|

|