Most Americans Are Still ‘Woefully Under-Saved’

Five years after the Great Recession, most Americans still haven’t established firm financial footing.

Only 22 percent of Americans have enough emergency savings to cover the recommended six months’ worth of expenses, according to a new report from Bankrate.com.

Of those surveyed, 21 percent had less than three months’ expenses saved.

Related: Americans Low Savings Rate a Bad Sign for Good Economy

“These results are further evidence that Americans remain woefully under-saved for unplanned expenses, and rather than progressing, are moving in the wrong direction,” Bankrate chief financial analyst Greg McBride said in a statement.

The number of Americans without any emergency savings reached a five-year high of 29 percent, up from 26 percent last year. Nearly a quarter of Americans said their savings had deteriorated in the past year.

Six months of emergency savings is the minimum amount recommended by many planners. Those with children or who have poor health or poor job security may need to an even larger emergency fund.

When an emergency hits those without an emergency fund, they often use credit cards or dip into retirement savings, both pricey options that can lead to further financial hardship.

A separate study released last month by BMO Harris Premier Services found that three quarters of consumers had dipped into their rainy day fund, with unexpected car and home repairs the most common reason cited.

Of those who had used emergency funds, about half replenished their savings within six months, while 20 percent never replaced the savings they had used.

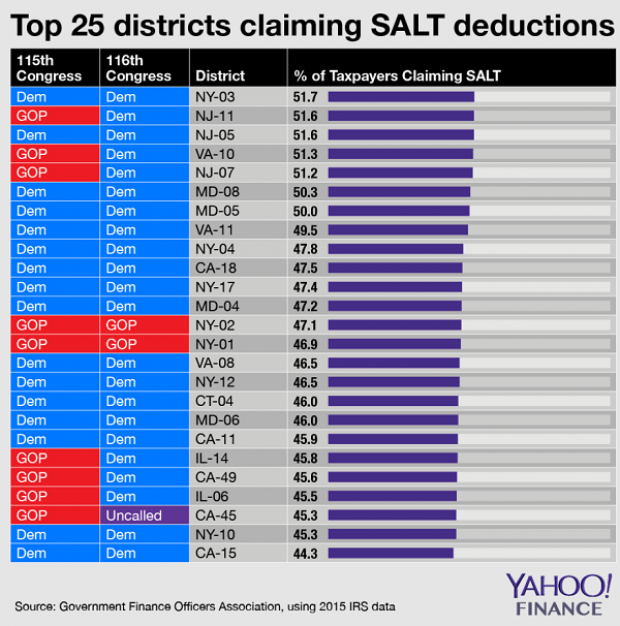

Chart of the Day: SALT in the GOP’s Wounds

The stark and growing divide between urban/suburban and rural districts was one big story in this year’s election results, with Democrats gaining seats in the House as a result of their success in suburban areas. The GOP tax law may have helped drive that trend, Yahoo Finance’s Brian Cheung notes.

The new tax law capped the amount of state and local tax deductions Americans can claim in their federal filings at $10,000. Congressional seats for nine of the top 25 districts where residents claim those SALT deductions were held by Republicans heading into Election Day. Six of the nine flipped to the Democrats in last week’s midterms.

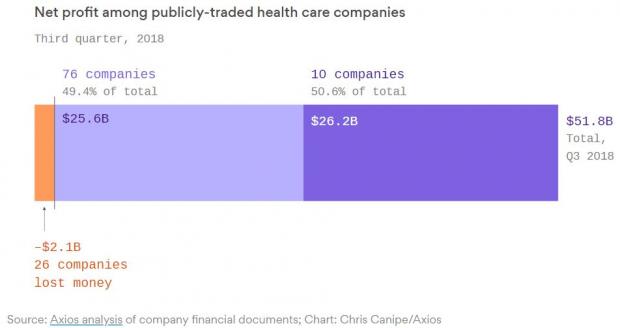

Chart of the Day: Big Pharma's Big Profits

Ten companies, including nine pharmaceutical giants, accounted for half of the health care industry's $50 billion in worldwide profits in the third quarter of 2018, according to an analysis by Axios’s Bob Herman. Drug companies generated 23 percent of the industry’s $636 billion in revenue — and 63 percent of the total profits. “Americans spend a lot more money on hospital and physician care than prescription drugs, but pharmaceutical companies pocket a lot more than other parts of the industry,” Herman writes.

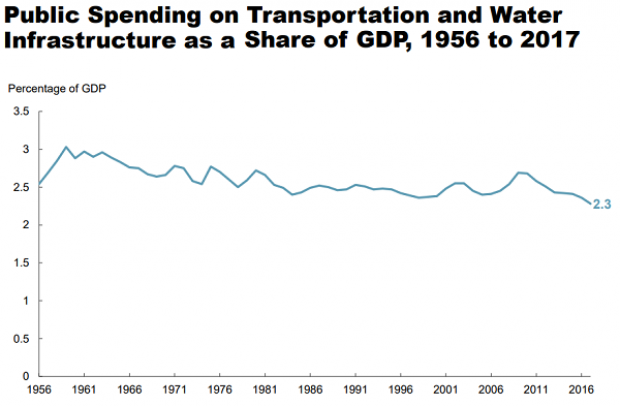

Chart of the Day: Infrastructure Spending Over 60 Years

Federal, state and local governments spent about $441 billion on infrastructure in 2017, with the money going toward highways, mass transit and rail, aviation, water transportation, water resources and water utilities. Measured as a percentage of GDP, total spending is a bit lower than it was 50 years ago. For more details, see this new report from the Congressional Budget Office.

Number of the Day: $3.3 Billion

The GOP tax cuts have provided a significant earnings boost for the big U.S. banks so far this year. Changes in the tax code “saved the nation’s six biggest banks $3.3 billion in the third quarter alone,” according to a Bloomberg report Thursday. The data is drawn from earnings reports from Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Wells Fargo.

Clarifying the Drop in Obamacare Premiums

We told you Thursday about the Trump administration’s announcement that average premiums for benchmark Obamacare plans will fall 1.5 percent next year, but analyst Charles Gaba says the story is a bit more complicated. According to Gaba’s calculations, average premiums for all individual health plans will rise next year by 3.1 percent.

The difference between the two figures is produced by two very different datasets. The Trump administration included only the second-lowest-cost Silver plans in 39 states in its analysis, while Gaba examined all individual plans sold in all 50 states.