The New Spider-Man: Sony and Marvel Bet Big on Tom Holland

After much speculation and debate, Marvel has finally revealed who will play Peter Parker in its next Spider-Man reboot — and it’s not a name you’ll be likely to recognize: 19-year-old Tom Holland.

Who? Exactly.

Significantly more cherubic than the last two stars cast in the role — Tobey Maguire and Andrew Garfield — Holland appeared in the 2012 movie The Impossible and had a stint in the title role of the London production of Billy Elliott. Now he’ll be the web-slinging superhero, starting with a relatively small role in next year’s Captain America: Civil War and then in an as-yet-unnamed Spider-Man movie.

Marvel had said they would be casting someone more in line with Spidey’s actual age. In the comics and films, Parker is ostensibly an 18-year-old high school senior, but Maguire was 27 when he first donned the mask, while Garfield was 28.

Related: Sony Spins a New Spider-Man Strategy with Disney

The very fact that Marvel was able to cast anyone in the role at all was thanks to a protracted negotiations with Spider-Man’s cinematic rights-holder, Sony. Finally clinching this deal allows Marvel to bring have Spider-Man play his pivotal and necessary role in Civil War, a comic-book story arc adored by critics and fans alike.

But as much as fans might have riding on Holland’s Spider-Man, Marvel and Sony are counting on him even more: They’re effectively betting hundreds of millions of dollars on the little-known actor, and hoping he can breathe new life into a franchise that, while is generated $1.5 billion in U.S. box office sales and about $4 billion worldwide, has seen dwindling returns over time.

The first Spider-Man movie starring Holland is slated to be released on July 28, 2017.

Spider-Man (2002): $403,706,375

Spider-Man 2 (2004): $373,585,825

Spider-Man 3 (2007): $336,530,303

The Amazing Spider-Man (2012): $262,030,663

The Amazing Spider-Man 2 (2014): $202,853,933

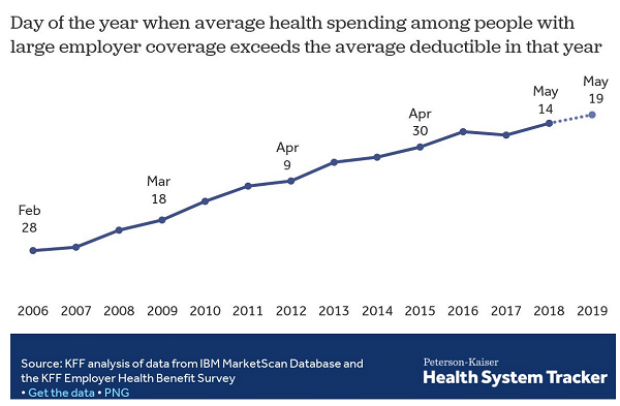

Coming Soon: Deductible Relief Day!

You may be familiar with the concept of Tax Freedom Day – the date on which you have earned enough to pay all of your taxes for the year. Focusing on a different kind of financial burden, analysts at the Kaiser Family Foundation have created Deductible Relief Day – the date on which people in employer-sponsored insurance plans have spent enough on health care to meet the average annual deductible.

Average deductibles have more than tripled over the last decade, forcing people to spend more out of pocket each year. As a result, Deductible Relief Day is “getting later and later in the year,” Kaiser’s Larry Levitt said in a tweet Thursday.

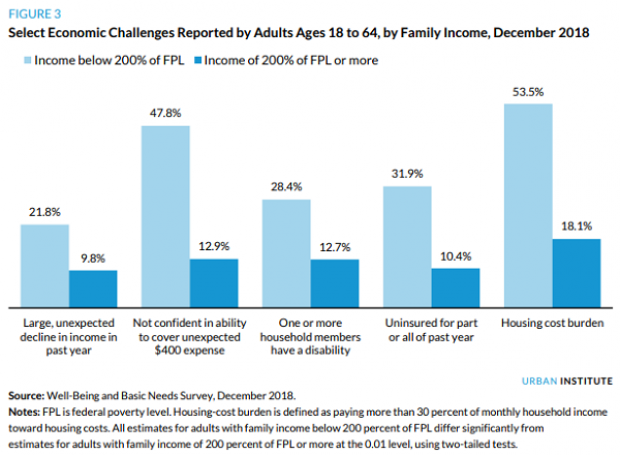

Chart of the Day: Families Still Struggling

Ten years into what will soon be the longest economic expansion in U.S. history, 40% of families say they are still struggling, according to a new report from the Urban Institute. “Nearly 4 in 10 nonelderly adults reported that in 2018, their families experienced material hardship—defined as trouble paying or being unable to pay for housing, utilities, food, or medical care at some point during the year—which was not significantly different from the share reporting these difficulties for the previous year,” the report says. “Among adults in families with incomes below twice the federal poverty level (FPL), over 60 percent reported at least one type of material hardship in 2018.”

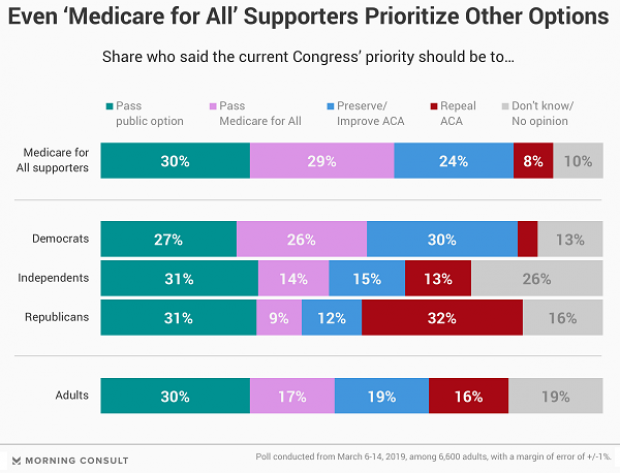

Chart of the Day: Pragmatism on a Public Option

A recent Morning Consult poll 3,073 U.S. adults who say they support Medicare for All shows that they are just as likely to back a public option that would allow Americans to buy into Medicare or Medicaid without eliminating private health insurance. “The data suggests that, in spite of the fervor for expanding health coverage, a majority of Medicare for All supporters, like all Americans, are leaning into their pragmatism in response to the current political climate — one which has left many skeptical that Capitol Hill can jolt into action on an ambitious proposal like Medicare for All quickly enough to wrangle the soaring costs of health care,” Morning Consult said.

Chart of the Day: The Explosive Growth of the EITC

The Earned Income Tax Credit, a refundable tax credit for low- to moderate-income workers, was established in 1975, with nominal claims of about $1.2 billion ($5.6 billion in 2016 dollars) in its first year. According to the Tax Policy Center, by 2016 “the total was $66.7 billion, almost 12 times larger in real terms.”

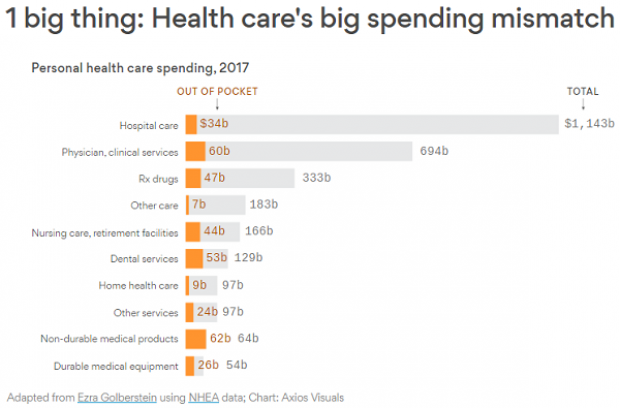

Chart of the Day: The Big Picture on Health Care Costs

“The health care services that rack up the highest out-of-pocket costs for patients aren't the same ones that cost the most to the health care system overall,” says Axios’s Caitlin Owens. That may distort our view of how the system works and how best to fix it. For example, Americans spend more out-of-pocket on dental services ($53 billion) than they do on hospital care ($34 billion), but the latter is a much larger part of national health care spending as a whole.