No less an authority than Donald Trump is fed up with our dependence on OPEC oil. In a recent interview hinting at a possible presidential bid, the real estate tycoon rages that “OPEC is setting the price of oil and ripping the lifeblood out of this country.”

Mr. Trump is not the only one concerned about our ongoing vulnerability to volatile oil prices. More ominously, the Chief Economist of the International Energy Agency (IEA) is warning that rising outlays for imported oil among OECD countries could trip up the global recovery. Faith Birol has reported that the cost of crude imports soared by $200 billion to $790 billion during 2010. This increase, stemming from higher prices and demand, equates to a 0.5% cut in income – a hefty penalty when the developed world is still struggling to regain its footing. Dr. Birol said “Oil prices are entering a dangerous zone for the global economy.”

With crude quotes hovering around $90 per barrel again, this threat is taking center stage. There is no question that oil price rises bring on recessions. A 2006 paper from the U.S. Energy Information Agency said, “most of the major economic downturns in the United States, Europe, and the Asia Pacific region since the 1970s have been preceded by sudden increases in crude oil prices.” The agency goes on to note that the cause and effect was less visible in the last decade, when “average world crude prices…increased by more than $30 per barrel…yet U.S. economic activity has remained robust, growing by approximately 2.8 percent per year from 2001 through 2004.” They had no idea what lay ahead.

in the average cost of imported oil, not from a collapse

in the value of subprime mortgages.

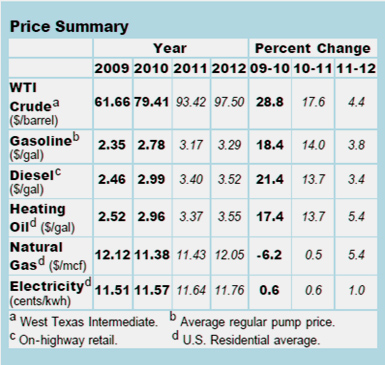

Some observers have suggested that the recent financial crisis had its roots in a jump in oil prices. James Hamilton of UC San Diego produced a report in 2009 saying that higher oil prices in 2007-2008 impacted domestic spending and auto purchases to such an extent that “in the absence of those declines, it is unlikely that we would have characterized the period 2007:Q4 to 2008:Q3 as one of economic recession for the U.S.” In other words, the Great Recession may have stemmed from a sharp jump in the average cost of imported oil, which rose from $59.05 per barrel in 2006 to $92.57 in 2008 – and not from a collapse in the value of subprime mortgages.

Since the 1960s consumer outlays on gasoline and heating fuel have ranged from a little below 5% in the late 1990s to nearly 10% in the early 1980s. When this ratio starts moving towards the higher end of the range, as it did in the mid- 2000s, the consumer cuts back on other spending, precipitating an economic downturn.

Though this relationship is well established, volatile oil prices are not an especially user-friendly predictive tool. Unexpected supply disruptions and geopolitical events can quickly move markets. For instance, in recent days a leak at a pumping station on the important Trans-Alaska pipeline and the closing of two Norwegian fields pushed crude above $90 a barrel, after reaching $95/bbl a week ago for the first time in nearly two years. At the end of 2008, the price of crude was a mere $34 per barrel.

in recent months pushes oil prices

to the point of dampening demand.

What lies ahead? As projections for world economic growth become slightly more bullish, estimates of future oil prices rise as well. For instance, in response to his firm’s modest bump up in GDP forecast (to 3.5% in 2011) Doug Terreson of International Strategy & Investment Group now projects oil prices this year and next will average $95 and $100 per barrel, respectively; formerly he was looking for $90 and $95 per barrel. Importantly, he expects demand to rise globally by 1.8 million barrels per day this year and by an additional 1.4 million barrels per day in 2012. In a recent call with clients, he points out that agencies such as the IEA are looking for more modest increases. If the industry is taken by surprise, production and inventory adjustments could lag the upward move in demand, ratcheting prices higher.

The risk is that the economic momentum we have seen in recent months pushes oil prices to the point of dampening demand. Terreson estimates that at $125 per barrel – a price we have breached before, “demand destruction” sets in. That’s analyst speak for – man the lifeboats, here we go again.

Presidents come and presidents go, and still the United States relies on imported oil. Since the 1970s we have learned that there is elasticity of demand for oil – that is, when prices zoom upward, demand craters. This is good news and bad news. True, the crisis of sky-high prices is consequently short-lived. On the other hand, just as our leaders are finally pushed to implement a sane energy policy that would embrace domestic oil production as well as all oil alternatives, green, brown and otherwise, the country hits a recession. Oil prices fall, voters become more concerned with jobs and incomes, and our leaders are off the hook until the process starts up again.

This is a sorry excuse for the continued lack of an energy policy. Being reliant on imported crude and the roller-coaster of global oil prices wreaks havoc on our economy over and over again. The best and most efficient starting point to diminish this vulnerability, in my view, would be the implementation of an oil import fee. Put a floor under the price of energy in this country, and let market forces determine the most economical alternatives. Investors in nuclear power plants or wind farms and other alternatives need to know that they will not be undercut by sharp drops in oil prices. The sacrifice paid by consumers in the short term will be repaid handsomely over time.

Who knows? Maybe Donald Trump will one day tell the Saudis: “You’re fired!”

Related Links:

Oil Prices Rally, Make Imports More Expensive (Forbes.com)

Oil Incentives That Might Actually Work? Dream On (Chron.com)