The raw numbers show very good times for the U.S. housing market, one of the bulwarks of support for economic growth. Existing home sales rose for the second straight month in April and are tracking 6 percent above last year. New home sales shot up at their fastest pace in eight years. Housing starts, building permits and pending home sales — a signal of future growth — are also all increasing at healthy clips.

It’s enough to make you believe that the housing market has completely left behind the troubles of the bubble and crash years and is poised to lead the nation into prosperity. But there’s something lurking in the data, which I first identified in my very first article at The Fiscal Times two years ago. We don’t have a housing market, we have two: one for the rich and one for the rest.

Related: Why a President Trump Could Hurt Your Home's Value

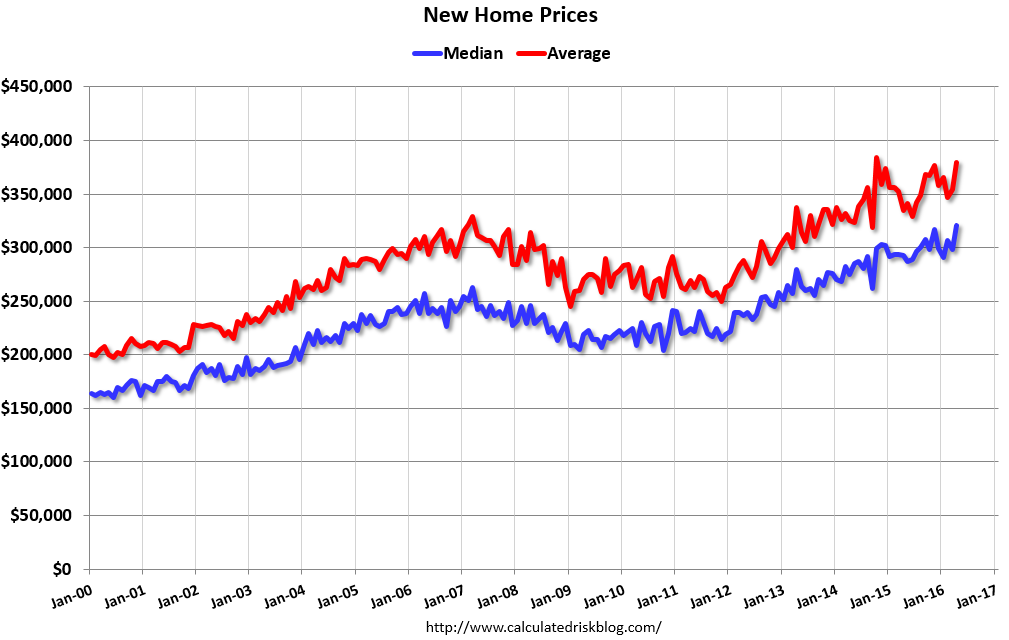

First of all, the supply of new and existing homes appears to be shrinking, a natural occurrence given that sales have risen. We can get out our supply and demand curves and reason that low inventory inevitably means higher prices. And indeed, the average sales price on a new home in April was $379,000 (the median price was $321,100, meaning 50 percent of sales were above that number and 50 percent were below).

This is a record in nominal dollars (though if you account for inflation, it’s only halfway up the scale of the housing bubble). And it reflects a change in the mix of home sales, which you can see in this quarterly sales chart from the U.S. Census Bureau. Though new homes sales rose from 2013-2015, sales of homes below $200,000 keep falling. And homes at the higher end, particularly those selling for $400,000 and over, are rising. According to Bill McBride of Calculated Risk, 30 percent of new homes sold in 2002 were under $150,000. In April, that number was 2 percent.

It’s clear that builders are making more luxurious homes rather than trying to attract entry-level buyers. Not only does this maximize their profits, it matches with the consumers most willing to buy homes.

Related: 10 Trends Driving the Housing Market Now

The conventional wisdom on this topic is that lower-income homeowners with subpar credit scores were being pushed out of the housing market by gun-shy lenders wary of new government regulations. They “closed the credit box” to newer borrowers, denying Americans their chance at a home. The Urban Institute estimated in 2014 that 1.2 million borrowers were denied credit from these tighter standards, and a disproportionate number of those were borrowers of color.

First of all, even the Urban Institute admits that the credit box has loosened in the past two years. Just this week, both JPMorgan Chase and Wells Fargo started offering mortgages with a skinny 3 percent down payment.

Second, take a look at this intriguing analysis from Archana Pradhan, an economist with market research firm CoreLogic. Pradhan looks at the data and finds that the problem is not tighter supply of mortgage credit, but weaker demand at the low end. The denial rate for loans is actually lower today than in 2005 and 2006, and the distribution of credit scores for loan applicants has shifted dramatically. Fewer people with poor credit scores are even bothering to apply for a mortgage. “Self-sidelining of cautious/discouraged consumers makes it appear as if credit is tightening,” Pradhan writes.

Related: Where Housing Sales Are Slowing as Prices Keep Rising

Maybe low credit-score borrowers are discouraged by the expectation of being denied a loan. But I think two other things are going on. First of all, people don’t have the money. Wages are starting to grow a bit but have been stagnant for years, and with prices growing, they simply cannot afford a mortgage. This is especially true among millennials; according to the Pew Research Center, for the first time since the 1880s, more young people aged 18-34 are living with a parent than with a spouse or romantic partner.

Besides the discouraged borrowers, there are the cautious ones. CoreLogic estimates that 6.2 million families have lost their homes to foreclosure since September 2008. Practically everyone in the middle class of this country either experienced the horrors of mortgage defaults, loan modification attempts and eviction notices or knows somebody who did.

A decade after the housing bubble started to collapse, people remain shattered by foreclosure or continue to fight for their homes. More than one in three homes valued at $100,000 are still “underwater,” meaning the borrower owes more than the home is worth. The foreclosure fiasco totally crushed families, and would-be buyers reasonably look at that mess and opt out.

Related: A Surprising Reason the Home Ownership Rate Is Falling

Low demand for entry-level or modestly priced homes fuels developer desires to maximize profits by catering to the luxury market, filled with the only people left buying. The whole thing folds on itself, accelerating the trend of wealthy Americans segregating themselves through housing and pulling away from everybody else. The most expensive zip codes in America have seen far greater price appreciation than their lower-income counterparts (this is particularly true when you factor in communities of color, where prices have stalled out the most). And the biggest factor in that price appreciation is higher demand: In higher-income areas, more people bid against one another on properties.

This divide has tremendous implications for the country.

First of all, home values remain one of the few ways for lower-income families to gain wealth in America. If they don’t want or don’t feel they can get a mortgage, we have to find other wealth-building strategies.

Second, the continuing trend toward the luxury market could create a price spiral that eats away at affordability, especially if mortgage interest rates rise.

Third, housing groups could continue to push to “open the credit box” when that isn’t the problem, exposing those vulnerable families willing to buy a home to more risk. And finally, the economy won’t expand as much if residential housing is a mere playground for the rich.

Related: Here’s a Good Reason to Worry About Trump’s Economic Policies

The situation is far worse in the rental markets, where affordability is at a point of crisis. Maybe more construction would help, or maybe regulators can generate more confidence that housing isn’t a trap for the non-rich. Or maybe people just need to have enough money to actually afford a home (which would help fix rental markets, too, by reducing demand). But until we unlock the keys to reversing this, and give everyone a shot at an affordable place to live, we cannot claim that the housing market is on stable footing.

{kind=link}

{kind=link}