4 Reasons the Fed Won’t Raise Interest Rates in June

It is no surprise that the Fed didn’t take action on interest rates at the April Federal Open Market Committee meeting. The question of interest to the market is whether the Federal Reserve has revealed some clear signal in its statement about the timing of the future rate increase. Even though the Fed did not change its forward guidance on rate increases from the March statement, we can discern what the Fed has on its plate. Four aspects of the economy stand out:

Related: Bernanke Was Right—Interest Rates Aren’t Going Anywhere

- The latest GDP data show worse-than-expected growth at an annualized 0.2 percent during the first quarter of 2015, compared to 2.2 percent in the last quarter of 2014.

- The strong U.S. dollar has continued to weigh on exports. Net exports in the first quarter stayed unchanged (0.0 percent growth) year-over-year, compared with 18.6 percent growth in the fourth quarter of 2014.

- Inflation has continued to stay way below the central bank’s 2 percent target. The price index for personal consumption expenditure (PCE), the measure of inflation preferred by the Fed, showed a 0.3 percent year-over-year increase in the first quarter, much lower than the growth rate of 1.1 percent in the fourth quarter of last year. Core PCE inflation, which excludes volatile prices of food and energy, reached 1.3 percent, compared with 1.4 percent in the last quarter.

- The improvements in the labor market, the other mandate of the Federal Reserve besides inflation, also slowed. Only 126,000 employees were added to nonfarm payrolls in March, compared to 264,000 in February and 201,000 in January.

Related: Fed’s Downgrade of Economic Outlooks Signals Later Rates Lift-Off

In all, the U.S. economy is growing more slowly than anticipated with some headwinds that may last for a while, such as the strong dollar. Both measures of the Fed’s dual mandate, price stability and maximum employment, remain below the Fed’s target. Normally this would call for an accommodative monetary policy, postponing the rate increases until later in the year. Rather than starting rate increases at the June FOMC meeting, the liftoff in September instead is more likely.

This story originally appeared at the American Institute for Economic Research.

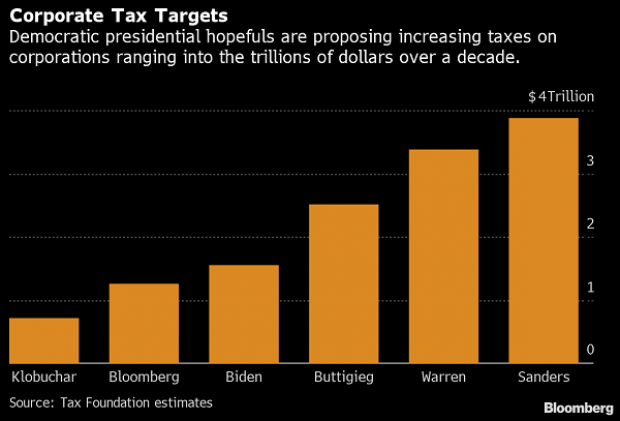

Chart of the Day: Boosting Corporate Tax Revenues

The leading candidates for the Democratic presidential nomination have all proposed increasing taxes on corporations, including raising income tax rates to levels ranging from 25% to 35%, up from the current 21% imposed by the Republican tax cuts in 2017. With Bernie Sanders leading the way at $3.9 trillion, here’s how much revenue the higher proposed corporate taxes, along with additional proposed surtaxes and reduced tax breaks, would generate over a decade, according to calculations by the right-leaning Tax Foundation, highlighted Wednesday by Bloomberg News.

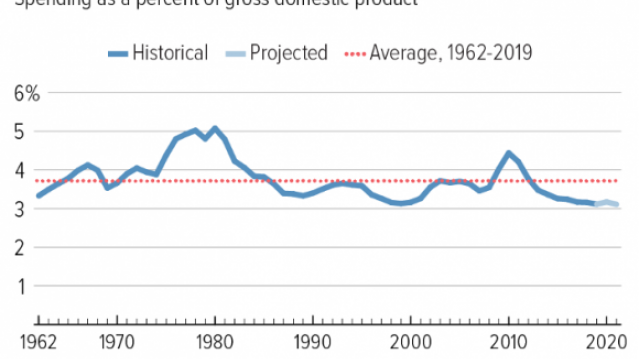

Chart of the Day: Discretionary Spending Droops

The federal government’s total non-defense discretionary spending – which covers everything from education and national parks to veterans’ medical care and low-income housing assistance – equals 3.2% of GDP in 2020, near historic lows going back to 1962, according to an analysis this week from the Center on Budget and Policy Priorities.

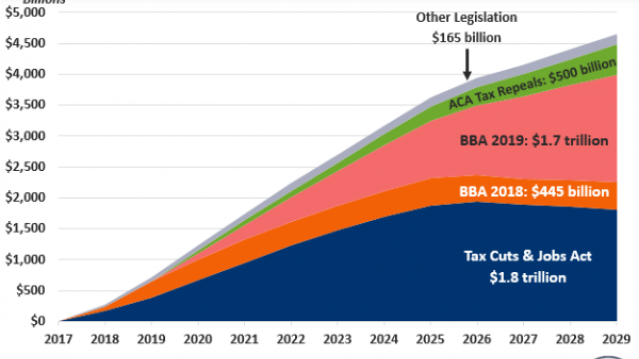

Chart of the Week: Trump Adds $4.7 Trillion in Debt

The Committee for a Responsible Federal Budget estimated this week that President Trump has now signed legislation that will add a total of $4.7 trillion to the national debt between 2017 and 2029. Tax cuts and spending increases account for similar portions of the projected increase, though if the individual tax cuts in the 2017 Republican overhaul are extended beyond their current expiration date at the end of 2025, they would add another $1 trillion in debt through 2029.

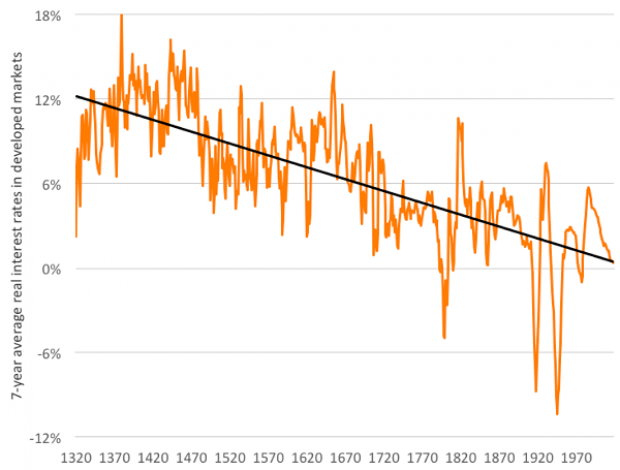

Chart of the Day: The Long Decline in Interest Rates

Are interest rates destined to move higher, increasing the cost of private and public debt? While many experts believe that higher rates are all but inevitable, historian Paul Schmelzing argues that today’s low-interest environment is consistent with a long-term trend stretching back 600 years.

The chart “shows a clear historical downtrend, with rates falling about 1% every 60 years to near zero today,” says Bloomberg’s Aaron Brown. “Rates do tend to revert to a mean, but that mean seems to be declining.”

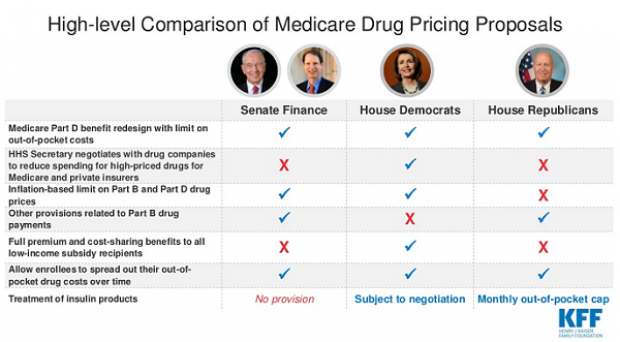

Chart of the Day: Drug Price Plans Compared

Lawmakers are considering three separate bills that are intended to reduce the cost of prescription drugs. Here’s an overview of the proposals, from a series of charts produced by the Kaiser Family Foundation this week. An interesting detail highlighted in another chart: 88% of voters – including 92% of Democrats and 85% of Republicans – want to give the government the power to negotiate prices with drug companies.